UK Dropshipper's 2026 Tax & VAT Survival Guide (with Free Tools)

UK Dropshipper's 2026 Tax & VAT Survival Guide (with Free Tools)

Quick answer: UK dropshippers face three tax pathways: under-£135 imports (AliExpress collects VAT at point of sale — you remit to HMRC if VAT-registered), over-£135 imports (you are usually the importer of record and owe import VAT plus duty), and marketplace-facilitated sales (marketplace handles VAT, you handle corporate tax on your margin); EU customers under €150 need IOSS registration to avoid customs delays.

UK dropshipping tax in 2026 is not as bad as it looks. There are three pathways, the rules under each are well-defined, and once you know which pathway your typical sale falls under you can put the recurring compliance work on autopilot. The hard part is figuring out which pathway applies, and the cost of getting it wrong is HMRC penalty letters that arrive 18-24 months after the fact.

This guide is the practical UK-dropshipper version. We are not a tax firm and nothing here is legal advice — for live filings you should pay a UK accountant who specialises in e-commerce. What we can do is map out the pathways, the trip-wires, and the toolset that handles the data-collection side of compliance so the accountant's job (and bill) shrinks.

1. The three ways UK dropshippers get taxed in 2026

A UK dropshipper sourcing from AliExpress and selling to UK and EU customers will encounter these three pathways. Most operators see all three across their order book in any given month.

Pathway A — Under-£135 imports from non-UK sellers

Since 1 January 2021, the UK has had a "low-value goods" import rule. Goods sold to a UK consumer with a value under £135, where the seller is outside the UK, fall under the rule. Under the rule, the marketplace or seller is responsible for collecting UK VAT at the point of sale, not the buyer at delivery. AliExpress applies UK VAT at checkout for orders shipped to UK addresses; the buyer pays VAT-inclusive at the moment of purchase.

For dropshippers, this means: when you place an order on AliExpress to fulfill a UK customer order, AliExpress has already collected the UK VAT on that supplier-side transaction. You as the dropshipper are buying VAT-inclusive from AliExpress and reselling to your UK customer. The customer-side transaction is your responsibility — you collect UK VAT from your customer at checkout and remit it to HMRC if you are VAT-registered.

The trip-wire: if you are not VAT-registered, you cannot legally charge VAT on your invoices, but you also cannot reclaim the input VAT on your supplier invoices. Below the £90,000 / 12-month VAT registration threshold (current as of 2026), you may not need to register voluntarily — but the maths often favours voluntary registration once you are doing meaningful AliExpress sourcing because the input-VAT reclaim is real.

Pathway B — Over-£135 imports

When the supplier-side order value exceeds £135, the under-£135 rule does not apply. You (the importer of record) become liable for import VAT and any applicable customs duty at the point the goods enter the UK. AliExpress will not collect UK VAT in advance because the rule does not cover this value tier.

Most dropship orders fall under £135 individually. The cases where you cross the threshold:

- High-value individual products (electronics, jewellery, watches) — single-item orders above £135 trigger the threshold.

- Bulk orders to your UK address for repackaging — if you are aggregating supplier shipments and re-fulfilling to customers, the import value is the supplier-shipment value, which crosses the threshold easily.

- Sample orders shipped in larger consolidations — sample-order strategies that aggregate items often cross the threshold.

The friction here is real. Customs delays, duty calculations, and HMRC correspondence add operational time. Most dropshippers structure their sourcing to stay under £135 per shipment specifically to avoid this pathway.

Pathway C — Marketplace-facilitated sales

If you sell on a marketplace that operates in the UK (eBay UK, Amazon UK, Etsy, OnBuy), the marketplace facilitator rules apply. Under these rules, the marketplace is responsible for collecting and remitting UK VAT on sales to UK consumers, not you. You receive your payout net of the marketplace's VAT collection.

For your accounting, this means: marketplace sales appear on your books at the gross figure (before marketplace VAT) for revenue reporting and at the net figure for cash-flow reconciliation. Your corporate tax (or self-employment income tax) is calculated on your margin after marketplace fees and VAT — not on the gross customer payment.

The trip-wire: marketplaces do not handle the supplier-side transaction. If you sourced an over-£135 product, you still owe the import VAT on the supplier side even though the marketplace handled the customer-side VAT. Operators who assume "marketplace handles it" without checking the sourcing-side liability get caught.

2. The HMRC trip-wires that catch dropshippers

Three patterns we see catch new UK dropshippers repeatedly.

Trip-wire 1: Operating as "I'm not really a business yet"

Until you formally register as self-employed or as a limited company, HMRC's default position is that any sustained income-generating activity is a business. The threshold for "sustained" is fuzzy — there is no specific revenue line. Operators running 50 orders a month for six months are clearly a business. HMRC's enforcement timeline tends to lag activity by 18-24 months, which is why so many operators get penalty letters in 2026 for activity in 2024 they had assumed was hobby-tier.

Register early. Self-assessment for sole traders is straightforward; limited company registration for >£30K profit is usually worth the structure once your numbers cross that line. Either way, "not really a business" is not a legal status; it is a delay.

Trip-wire 2: Misclassifying who the importer is

The importer-of-record question matters because the importer pays import VAT. Dropshippers often assume the customer is the importer because the package is shipped to the customer's address. This is sometimes correct (under-£135 + AliExpress collected VAT) and sometimes wrong (over-£135, or you operate the supplier account in your name).

When in doubt, the safe position is: if your AliExpress account is shipping to your UK customer and the value exceeds £135, you are typically the importer and you owe the import VAT. Build this into your pricing model. Operators who ignore this end up with surprise £200-1,500 customs invoices on edge-case orders.

Trip-wire 3: Not capturing the data trail

HMRC compliance is data-driven. When you face an enquiry, the question is not "did you do the right thing?" — it is "can you document that you did the right thing?" Operators who do not retain supplier invoices, marketplace payout statements, customs documentation, and import VAT receipts have a much harder time defending their numbers than operators who do.

The data-trail tools below cover this layer.

3. IOSS / OSS for selling to EU customers

If your UK store also ships to EU customers (a common pattern post-Brexit because cross-border EU traffic is still meaningful), the EU's Import One-Stop Shop (IOSS) rules apply.

IOSS allows you to register once in the UK (or via a fiscal representative) and remit VAT on under-€150 sales to all 27 EU member states through a single quarterly return. Without IOSS, the EU customer pays VAT plus a customs handling fee at delivery, which is a poor customer experience and depresses conversion rates.

The two practical scenarios:

- You sell low-volume to EU customers: IOSS registration may not be worth the setup cost. Accept the worse customer experience or geo-restrict your EU traffic.

- You sell meaningful volume to EU customers: IOSS registration is a clear win. The setup is one-off; the quarterly returns are routine; the customer-experience improvement is large.

The OSS scheme (One-Stop Shop) covers EU-domestic sales above €10K cross-border per year. Most UK dropshippers will not hit OSS thresholds, but if you are doing high-volume to one specific EU country, talk to an accountant about whether OSS applies.

4. The four-tool stack to automate the recurring work

The tax pathways above are the one-time learning curve. The recurring work — capturing the data trail, classifying orders by pathway, monitoring supplier-side risk for tax-affecting issues — is where automation matters. Four tools cover most of the recurring work and three of the four are free.

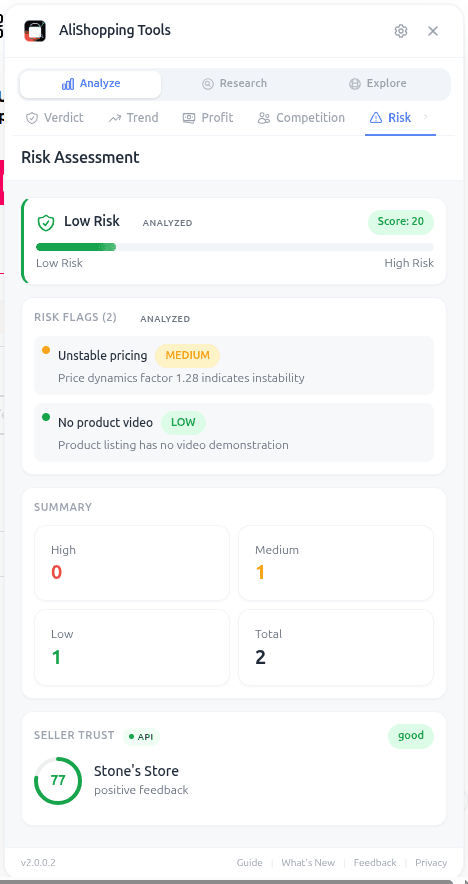

Tool 1: AliShopping Tools (free) — supplier-risk and price-history capture

The AStools Chrome extension surfaces supplier-side data on every AliExpress product page: the supplier name, the supplier rating, the price history, the dispute rate, the listing-stability signals. For UK dropshippers this matters specifically because:

- Supplier-side disputes that lead to refunds reverse the supplier-side import-VAT calculation. The risk panel flags suppliers with above-threshold dispute rates so you can avoid building tax-data trails on suppliers who will require refund reversals.

- Price history on AliExpress listings matters when documenting your input cost for HMRC. Suppliers occasionally raise prices retroactively and capturing the original purchase-time price is part of the data trail.

For the deeper supplier-risk methodology, our supplier risk check guide and the 2026 supplier risk update cover the full scoring framework.

Tool 2: A UK-focused tax calculator (third-party)

Third-party tax calculators (we are not promoting a specific one — search for "UK e-commerce VAT calculator 2026" and pick one with HMRC-aligned methodology) handle the per-order pathway classification. Input the order value, the supplier country, the customer country, and the marketplace (if any), and the calculator outputs which pathway applies and what your VAT obligation is.

The good ones integrate with Shopify and pull order data automatically. The free ones are spreadsheet-based and require manual input. Either is acceptable — the principle is to classify every order at the moment it ships, not at the year-end self-assessment.

Tool 3: A bookkeeping tool that handles VAT (free or low-cost)

Bookkeeping tools (FreeAgent, QuickBooks Self-Employed, FreshBooks) include VAT handling for UK businesses. The free tiers cover sole traders below the VAT threshold; paid tiers from £5-15 / month cover VAT-registered businesses. The output is the quarterly VAT return that HMRC needs.

The data flow: Shopify orders → bookkeeping tool → quarterly VAT return. Capturing supplier-side input VAT (when you can reclaim it) requires importing AliExpress invoices into the bookkeeping tool — most of the tools have an import path for this.

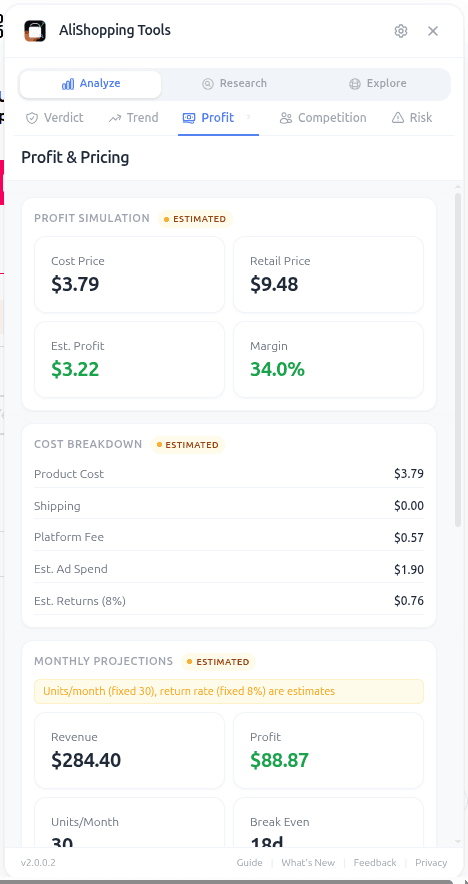

Tool 4: A profit-margin model that includes UK tax overhead

UK dropshippers often calibrate margins to numbers that ignore VAT. A 30% margin pre-VAT is a 25% margin post-VAT once you account for non-reclaimable elements. Building UK tax overhead into your profit model from the start avoids the surprise of running unprofitable on a model that "should have been" profitable.

The AStools profit simulator handles per-order margin including supplier-side VAT capture. For the full margin-modelling workflow, our profit calculator workflow guide walks through the line-by-line on a real product.

5. Quarterly compliance checklist

Run this checklist every quarter. It takes 30-60 minutes if your data is clean and gets faster as you build the habit.

- Pull all supplier invoices for the quarter (AliExpress order export, AutoDS / DSers reports, any direct supplier invoices). Verify each shows the supplier-collected VAT amount.

- Classify each order by pathway — under-£135, over-£135, marketplace-facilitated. Most orders should classify cleanly; flag any that do not for accountant review.

- Reconcile customer-side VAT collected — Shopify reports → bookkeeping tool. Verify the VAT collected ties to the orders shipped.

- Pull marketplace VAT statements (eBay, Amazon, Etsy) if you sell on those. The marketplace's VAT statement is your evidence for those orders.

- Capture supplier-side disputes and refunds for the quarter. Refund-affected orders need VAT reversals on both the supplier-input and customer-output sides.

- Verify UK winning products supply chain — for products you are scaling, our UK winning products guide covers the candidates that work specifically for UK customer demand. Verifying supplier reliability before scaling avoids tax-trail mess from supplier-side disputes.

- Cross-check against the trust signals — products with high refund rates carry compounding tax-trail mess. Our AliExpress trust hub covers the upfront verification that prevents most of this.

- Submit VAT return if VAT-registered. File on time; HMRC penalties for late filing scale fast.

- Archive the quarter — supplier invoices, marketplace statements, bookkeeping export. HMRC requires retention for at least 6 years.

6. The honest summary

UK dropshipping tax in 2026 is straightforward in principle and detailed in practice. The principle: there are three pathways, you classify each order to a pathway, you collect and remit the right VAT on the right side, and you keep the data trail. The detail: getting each step right consistently across hundreds of orders requires tooling, not willpower.

The four-tool stack above does most of the recurring work for £0-£20 / month total. For UK operators just starting out, this is the lowest-cost compliance stack we have seen work — and the alternative (manual tracking, surprise penalty letters) is far more expensive in money and time.

For broader free-tool coverage of the dropshipping research stack — supplier risk, profit modelling, and reading a listing's review evidence for yourself — our best free tools roundup covers the broader Chrome-extension layer that complements the tax-specific tools above, and the dropshipping product research guide is the pillar that ties product-validation discipline to UK dropshipping VAT compliance — both decide whether the next quarter is profitable or not.

Install AliShopping Tools free from the Chrome Web Store — covers supplier risk, price history, and profit simulation on every AliExpress product page. Free, no account, no signup. The first tool of the four-tool tax-trail stack.

For live filings, pay a UK e-commerce accountant. The £400-1,200 / year cost of a competent accountant is one of the highest-ROI line items on a UK dropshipper's P&L.

Disclosure: This article is published by the AliShopping Tools team. UK VAT rules cited are based on HMRC publicly available guidance as of April 2026. Rules change — verify current HMRC guidance before filing. Nothing in this article is legal or tax advice; consult a qualified UK accountant for live filings. Email feedback via contact page.

All trademarks referenced are the property of their respective owners. This guide is for educational purposes only.

Ready to find winning products?

Try AliShopping Tools — 15 free AI tools for product research.

Quick answers

Frequently Asked Questions

1How does VAT work for UK dropshippers in 2026?

UK dropshippers face three tax pathways: for imports under £135, AliExpress collects VAT at point of sale; for imports over £135, the dropshipper is typically the importer of record and owes import VAT plus duty; for marketplace-facilitated sales (Etsy, eBay, Amazon UK), the marketplace handles VAT and you handle corporate tax on your margin.

2When does a UK dropshipper need to register for VAT?

UK VAT registration is required once your total taxable turnover exceeds £90,000 in a rolling 12-month period (the 2026 threshold).

Below that threshold, registration is optional but may be beneficial if you want to reclaim input VAT on business costs.

Exceeding the threshold without registering results in penalties from HMRC.

3What is IOSS and does it apply to UK dropshippers?

IOSS (Import One-Stop Shop) applies to EU-destined goods only — not UK.

Post-Brexit, the UK operates its own import VAT system.

IOSS registration is relevant when you sell to EU customers: orders under €150 can use IOSS to collect VAT at checkout, preventing customers from paying VAT at the border.

4What happens when AliExpress ships over £135 to UK customers?

For packages declared over £135 shipped directly to UK customers, UK import VAT (20 percent) plus applicable customs duty applies at the border.

The liability typically falls on the importer of record — which for dropshipping may be either you or the customer depending on DDP versus DAP shipping terms.

Clarify DDP or DAP status with your supplier before listing.

5How is corporation tax calculated on the profit I keep from marketplace‑facilitated dropshipping sales?

For marketplace‑facilitated dropshipping, you only pay corporation tax on the net profit you retain after the marketplace deducts its fees and the VAT it collects on your behalf.

The current corporation tax rate is 25% for profits earned on or after 1 April 2024, and you must file a company tax return within 12 months of the accounting period’s end.

Keep a clear ledger of gross sales, marketplace commissions, and VAT collected, then apply the 25% rate to the remaining margin.

Accurate bookkeeping lets you claim allowable expenses and avoid over‑paying HMRC.

6What penalties does HMRC impose if I forget to pay import VAT on orders over £135?

If you fail to account for import VAT on shipments exceeding £135, HMRC can charge penalties and statutory interest on the unpaid tax — the exact penalty depends on whether the error was careless or deliberate.

Respond promptly to any penalty notice, since ignoring it typically leads to further enforcement action.

There's no AliShopping Tools feature that automatically flags orders above the threshold or generates VAT entries for you — that's something you (or your accounting software/bookkeeper) need to track manually, ideally by flagging any order over £135 at the point of sale.

7Which free tools can I use to automate my quarterly VAT returns as a UK dropshipper?

There's no single free, fully-automated pipeline that files your quarterly VAT return for you — AliShopping Tools helps with product sourcing and margin research, not VAT filing.

For UK VAT returns you'll typically need HMRC-recognized Making Tax Digital (MTD) software; several UK accounting platforms offer free or low-cost tiers for small sellers.

Check HMRC's list of recognized MTD software providers directly rather than assuming a specific free stack exists, since providers and their pricing change.

8Can I reclaim the import VAT I paid on orders above £135, and how long do I have to do it?

Yes—you can reclaim import VAT paid on >£135 shipments by including the amount on your next VAT return as a recoverable input tax, provided you hold the original customs documentation.

HMRC allows you to submit a refund claim for up to four years after the tax was incurred, but it must be recorded on the VAT return for the period in which the import VAT was paid, typically within 30 days of the payment date.

Ensure you keep the import VAT receipt, shipping invoice, and any duty statements; these will be required if HMRC audits the claim.

AliExpress handles VAT for under‑£135 orders, so only the >£135 imports need this reclaim process.

9What records must I keep for HMRC audits as a UK dropshipper in 2026, and for how long?

HMRC requires UK businesses to retain relevant transaction and customs records — sales invoices, supplier purchase orders, shipping labels, import VAT receipts, duty statements, and correspondence with marketplaces or customs authorities — for several years; check HMRC's current guidance for the exact retention period that applies to your business, since rules can change.

Digital copies are acceptable if legible and securely backed up.

AliShopping Tools doesn't have a document storage or archival feature — use your accounting software or a dedicated cloud storage system to keep these records organized.

More from the blog

Winning Products UK 2026: 10 Dropshipping Picks

10 dropshipping product categories for the UK market in 2026 — calibrated to Royal Mail economics, UK ad CPMs, and the British seasonal calendar, plus how to vet each candidate in AStools.

AliExpress Shipping to the UK: Delivery Times, VAT & Customs (2026)

How long AliExpress takes to reach the UK, how 20% VAT and post-Brexit customs work, and which shipping method is fastest for UK shoppers in 2026.

AliExpress vs All Platforms 2026: Ultimate Comparison

AliExpress vs Alibaba, Temu, DHgate, CJ Dropshipping, Zendrop, and Shein: 2026 guide to shipping, pricing, dropshipping, and which platform wins your use case.