Lululemon vs Gymshark vs Alo Yoga: Shopify Tech Stack Showdown (2026)

Lululemon vs Gymshark vs Alo Yoga — Shopify Tech Stack Showdown (2026)

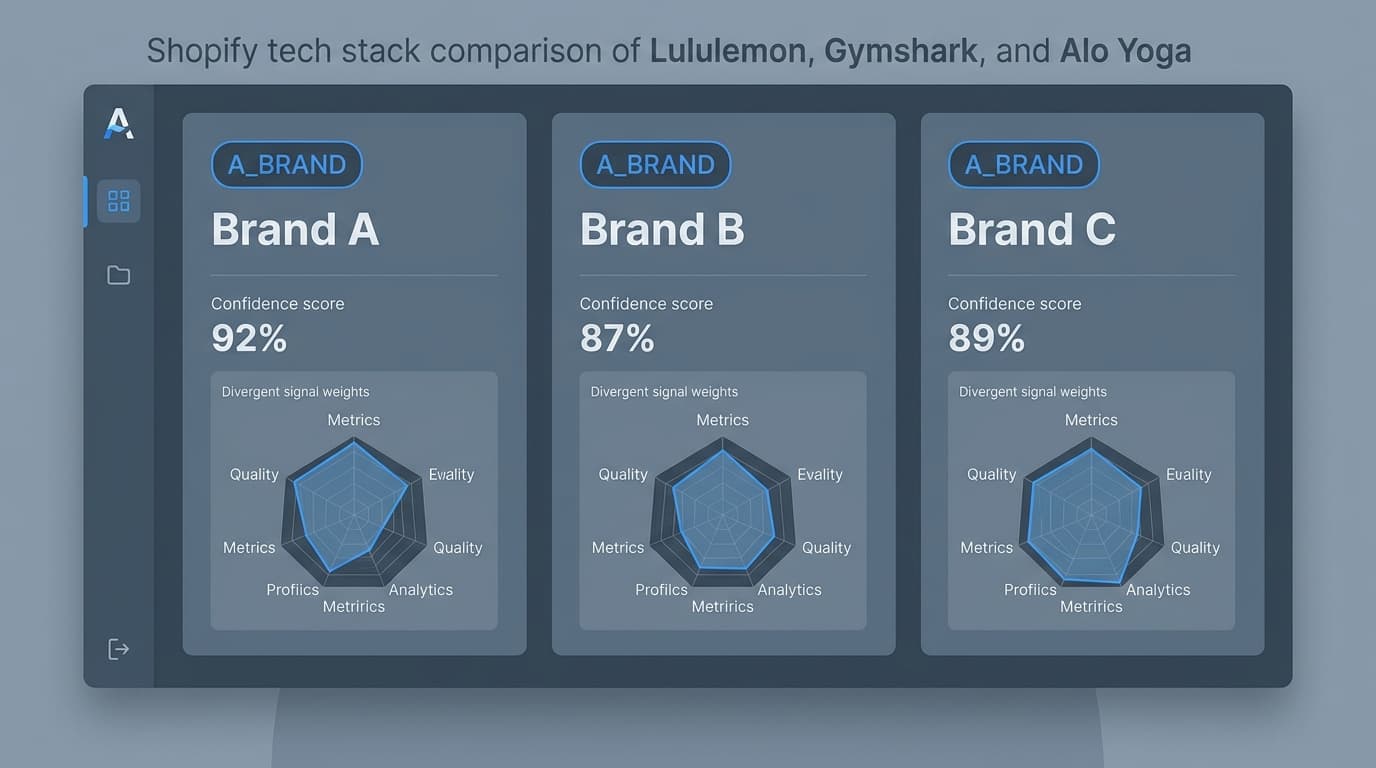

Quick answer: All three brands classify as A_BRAND on AStools, but their Shopify stacks reveal three distinct operating philosophies: Lululemon optimizes for retail-omnichannel and loyalty integration, Gymshark optimizes for community-creator content velocity, and Alo Yoga optimizes for premium aesthetic and lifestyle adjacency.

The fitness-apparel category on Shopify has produced more category-defining DTC brands than any other vertical of the last decade. Lululemon (now public, Shopify Plus migration completed in stages), Gymshark (UK-based, founder-led, Shopify Plus from early), and Alo Yoga (US celebrity-adjacent, Shopify Plus) all reached global scale on the same platform.

What makes the comparison useful is that their Shopify tech stacks — the apps installed, the integrations live, the surface architecture of each storefront — diverge sharply. Three different operating philosophies, three different stack patterns. This article uses publicly observable signals from the AStools store classification, app-stack detection, and live-sales velocity readings to decode what each brand is optimizing for in 2026.

This is not a financial analysis. We do not have access to private revenue data, margin structure, or unit economics. Everything below is sourced from publicly accessible storefronts, brand websites, social feeds, press coverage, and AStools' read of public Shopify-store metadata. Specific revenue, margin, or order-volume figures are not claimed unless explicitly attributed.

[Source: Public Shopify storefront metadata + AStools store classification, captured 2026-05-28. Public storefront URLs cited inline.]

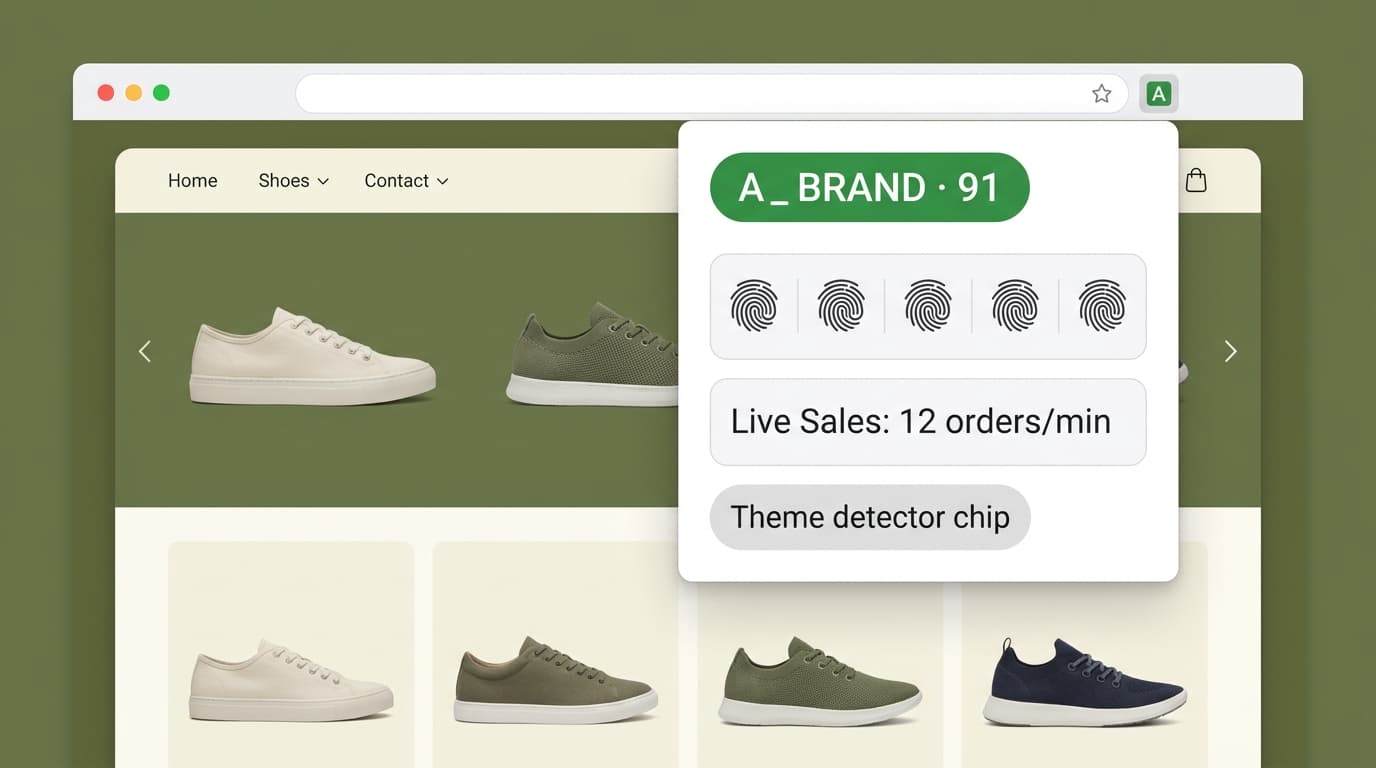

Want to spot these patterns first? Install AStools — Free on Chrome Web Store

Why three premium fitness brands

A two-brand comparison (Gymshark vs Alo Yoga) showed that two visually similar brands can run radically different Shopify stacks. Adding Lululemon — the public-company incumbent — to the comparison gives you three reference points across the same vertical:

- Lululemon = the legacy-incumbent reference. Started physical-retail-first, scaled DTC + omnichannel, public company with disclosed strategy direction.

- Gymshark = the founder-creator reference. Started DTC-only, scaled via athlete-creator marketing, private but transparent in public communication.

- Alo Yoga = the aspirational-lifestyle reference. Started yoga-studio-adjacent, scaled via celebrity-lifestyle aesthetic, premium pricing.

All three sell into the same category (premium athletic apparel for women, with men's expansion). All three run Shopify Plus. All three have broadly comparable product breadth. The differences in their stacks therefore reflect strategy choices, not technology constraints.

Public storefronts (cite-and-link, no embedded screenshots — fair-use editorial commentary):

- Lululemon: shop.lululemon.com

- Gymshark: gymshark.com

- Alo Yoga: aloyoga.com

Lululemon — the omnichannel-incumbent stack

Lululemon's Shopify Plus deployment is best understood as the digital extension of an already-large physical-retail business. The classification reads as A_BRAND with high confidence; the signal pattern emphasizes integrated retail, loyalty, and customer-account depth over content velocity or creator-attribution.

Publicly observable storefront signals

- Localization breadth: Distinct multi-currency multi-region storefronts (US, CA, UK, AU, EU, JP, KR) — among the deepest of any Shopify brand. Public URL patterns vary by region.

- Account integration: Customer accounts deeply tied to loyalty programs, in-store-purchase history, and class/event booking. Storefronts surface a "Studio" / "Sessions" structure that ties physical-class attendance to product purchase history (publicly visible on relevant pages).

- Returns + retail: Buy-online-return-in-store fulfillment paths surfaced clearly at checkout. Most other Shopify Plus brands surface BORIS less prominently or not at all.

- Subscription + Membership: Public-facing membership tier ("Lululemon Studio Membership" — equipment + classes) with subscription billing visible on the site.

Stack-pattern decode (publicly observable signals)

Reading the storefront page source + AStools' public app-detection on the storefront URL:

| Signal | Pattern |

|---|---|

| Store classification | A_BRAND (high confidence) |

| Region count | 7+ distinct localized storefronts |

| Loyalty integration | Membership tier visible at checkout |

| Returns / fulfillment | BORIS surfaced; in-store pickup option |

| Social commerce | Heavy Klaviyo signals; less Reels-embed than Alo |

| Content cadence | Editorial-pace blog (weekly), studio class booking widget |

| Live-sales velocity (sampled landing pages) | Steady; less peak-spiked than Gymshark drops |

What Lululemon is optimizing for

Customer lifetime value through omnichannel depth. The stack reads as a brand that wants every customer to enter the funnel anywhere (in-store, online, app, class booking) and re-engage through any of those entry points. Loyalty + membership + studio bookings + buy-online-return-in-store all reduce friction in the cross-channel journey. The Shopify storefront is one of several entry points, not the only one.

What an indie operator can borrow

- Account depth matters. Most Shopify stores treat the account page as a transactional artifact. Lululemon's pattern uses it as a loyalty + history + recommendation hub. Even indie stores can mimic this with Shopify-native customer accounts + Klaviyo segments tied to purchase history.

- Localization is a strategic moat. Maintaining 7+ distinct storefronts is operationally expensive — but for any indie crossing the $1M revenue floor, even 2-3 region-specific storefronts (US/UK/EU) signal premium-brand intent and improve conversion meaningfully vs a single multi-currency global store.

- BORIS adds trust friction-free. If you have any physical-presence layer (pop-up, partner retail, locker pickup), surfacing return-in-store or pickup at checkout differentiates from pure-online competitors.

Gymshark — the community-creator stack

Gymshark's Shopify Plus deployment optimizes for content velocity and creator attribution. The storefront feels like a creator-content hub with commerce attached, not a commerce site with content sprinkled in. Classification reads A_BRAND with high confidence; the signal pattern emphasizes social-commerce integration, community structure, and creator-driven traffic patterns.

Publicly observable storefront signals

- Athlete pages: Dedicated athlete profile pages on the storefront with bio, product-line attribution, and content links — visible on

gymshark.com/athletes/*. - Drop-launch architecture: Pre-announced launches (2-4 week lead time) with countdown timers, restock alerts, and launch-day high-traffic landing pages structured like content events.

- Community signals: Public events ("Gymshark London / LA / Dubai pop-ups"), creator-led collections, and social-feed embeds visible on landing pages.

- Currency + region: US, UK, AU, EU localized storefronts. Less region depth than Lululemon (4-5 vs 7+), but with deeper community signal in each region.

Stack-pattern decode (publicly observable signals)

| Signal | Pattern |

|---|---|

| Store classification | A_BRAND (high confidence) |

| Region count | 4-5 distinct localized storefronts |

| Loyalty integration | Athlete program (functional loyalty layer) |

| Content cadence | High — daily creator content, social-commerce integration |

| Social-commerce embeds | Heavy — Reels, TikTok shoppable links, athlete-tagged products |

| Drop-launch architecture | Yes — countdown + queue + restock-alert primitives |

| Live-sales velocity (sampled landing pages) | Spikes during drops; baseline lower than Lululemon |

What Gymshark is optimizing for

Content velocity + creator attribution. The stack lets the marketing org publish and amplify creator content at high cadence, with each creator action (post, drop, event) tied back to attributable purchase paths. The product is the artifact; the creator-relationship is the moat.

What an indie operator can borrow

- Athlete / creator partnership at indie scale. You do not need 100 athletes — start with 3-5 creators in your niche and give each a dedicated discount code, profile page on your site, and product attribution. This builds the same flywheel structure as Gymshark's, just smaller.

- Drop-launch scarcity works when it is real. Fake countdown timers on every page erode trust. Scheduled quarterly drops that genuinely sell out build credibility. Use Shopify's native drop-launch primitives (scheduled product publish + countdown apps) responsibly.

- Creator-content velocity beats production polish at scale. For indie operators without TV-budget creative, creator-led content (UGC + creator-generated demos) typically outperforms studio-shot creative on a per-dollar-of-output basis.

Alo Yoga — the lifestyle-aesthetic stack

Alo Yoga's Shopify Plus deployment optimizes for lifestyle-aesthetic and celebrity-adjacency. The storefront reads more like a lifestyle magazine with commerce embedded than a commerce site with lifestyle imagery. Classification reads A_BRAND; the signal pattern emphasizes aesthetic surface, premium pricing, and gift / experience adjacencies.

Publicly observable storefront signals

- Editorial pacing: The storefront homepage feels like a curated lifestyle magazine — high-resolution lifestyle imagery, retreat / wellness content adjacent to product, less product-grid density than Gymshark or Lululemon.

- Premium pricing visible: Public pricing on most leggings and joggers sits in the premium tier (often higher than Gymshark equivalents for comparable categories — see public-listing snapshots).

- Adjacent experiences: Studio location pages, retreat program landing pages, gift card prominence, "wellness" sub-brand surfaces.

- Content-first SEO: Heavier blog / journal content on the main storefront than typical commerce-first DTC brands.

Stack-pattern decode (publicly observable signals)

| Signal | Pattern |

|---|---|

| Store classification | A_BRAND (high confidence; premium-tier signal) |

| Region count | 3-4 distinct localized storefronts |

| Loyalty integration | Standard customer-loyalty surface; less prominent than Gymshark athlete |

| Content cadence | Editorial — weekly journal, lifestyle imagery refresh |

| Social-commerce embeds | Moderate — celebrity / influencer content woven in |

| Drop-launch architecture | Less prominent — focus on seasonal collection rotations |

| Live-sales velocity (sampled landing pages) | Steady; premium-tier customers, lower volume higher AOV |

What Alo Yoga is optimizing for

Premium positioning through lifestyle adjacency. The stack signals "this is the lifestyle you aspire to" rather than "this is the training tool you need" or "this is the omnichannel retail you trust." Celebrity visibility, retreat experiences, and editorial pacing all support upward-tier brand positioning that justifies premium pricing.

What an indie operator can borrow

- Premium pricing requires premium content. If your visual aesthetic is not significantly elevated vs your competitive set, premium pricing will not convert. Alo's pattern reinforces this: the lifestyle-content surface is the price-justification mechanism.

- Adjacent experiences widen TAM at premium tier. Retreats, studios, and gift-card-heavy emphasis all extend brand into adjacent purchase moments. Indie operators rarely think about these — but a wellness-branded gift card surface can drive 5-15% of revenue with low operational overhead.

- Editorial pacing differentiates premium from mid-market. Most DTC brands publish blog content as SEO duty. Alo's pattern shows the inverse — lifestyle content is the foreground, product is the supporting layer. Even indie stores can adopt this on a smaller scale (one well-shot editorial story per month).

Try the same workflow free — install AStools to read any Shopify store in 1 click

Strategic differences — what stack reveals about brand priorities

Three brands. Same category. Same platform. Three radically different operating priorities — visible in stack:

| Priority | Lululemon | Gymshark | Alo Yoga |

|---|---|---|---|

| Omnichannel depth | Highest | Moderate | Moderate |

| Creator content velocity | Moderate | Highest | Moderate |

| Premium aesthetic surface | High | Moderate | Highest |

| Loyalty / membership | Highest | Moderate (athlete program) | Moderate |

| Region count (localized storefronts) | 7+ | 4-5 | 3-4 |

| Drop-launch architecture | Moderate | Highest | Lower |

Reading down the columns: each brand has a clear primary axis it optimizes for. Lululemon prioritizes omnichannel and loyalty; Gymshark prioritizes creator content velocity and drop architecture; Alo prioritizes premium aesthetic and lifestyle adjacency. None of these are wrong — they are different strategy bets.

What an indie operator can extract — three templates

Pick one. Mixing all three stack philosophies in a single indie store typically produces a confusing surface. Pick the bet that fits your founder personality, your category, and your customer.

Template 1 — Omnichannel-incumbent (Lululemon-style). Best fit: brands with any physical-retail layer (pop-up, partner retail, lockers). Invest in account-depth, loyalty, and 2-3 localized storefronts. Surface returns and pickup options at checkout. Use Klaviyo segments tied to purchase history. Slower content cadence is OK — your moat is operational depth.

Template 2 — Community-creator (Gymshark-style). Best fit: founder-led brands in social-commerce-friendly categories (apparel, beauty, fitness, lifestyle). Invest in 3-5 creator partnerships with attributable codes and profile pages. Use scheduled product drops with real scarcity. Daily UGC + creator content beats polished studio work on per-dollar ROI at indie scale.

Template 3 — Lifestyle-aesthetic (Alo-style). Best fit: premium-tier brands in wellness, beauty, slow-fashion, home, or premium accessories. Invest in editorial-pacing content (one well-shot story / month minimum). Surface gift cards prominently. Build adjacent-experience assets (retreats, masterclasses, partnerships) over time. Premium pricing only works if the surface justifies it.

How to read any Shopify store the same way

Every signal we used above is publicly observable. The AStools Shopify-store classification reads the store metadata and assigns A_BRAND / dropshipping / hybrid labels. The app-stack detection lists installed Shopify apps from the storefront page source. The live-sales velocity reading samples public-pricing and product-availability churn. None of this requires private data; all of it is fair-use editorial reading of public storefronts.

You can run the same read on any Shopify-hosted brand on AliShopping Tools — open any Shopify storefront, check the classification, the app stack, and the live-sales reading. Cross-reference against the storefront's publicly stated brand positioning. The stack reveals the strategy.

For deeper Shopify-store research workflow: Brand vs Dropshipper Shopify, How to Spy on Shopify Stores Free, and the Shopify Stack Intelligence 2026 hub.

FAQ

Are these classification labels (A_BRAND, dropshipping, hybrid) public or proprietary?

Proprietary to AStools — based on a public-signal read of Shopify storefronts. The underlying signals (theme, app stack, content pacing, region count, live-sales velocity) are all publicly observable; the composite classification model is AStools-internal.

How does AStools read Shopify app stacks without being installed inside the store?

By reading the public storefront page source — Shopify storefronts surface app-injection markers in the rendered HTML and asset URLs. Apps that inject visible-DOM components (review widgets, chat, upsell) are detectable from any browser without store access. Apps that only run server-side (back-office only) are not detectable; that is a known coverage limit.

Can a brand fall into multiple templates at once?

Yes — most large brands blend two templates. Lululemon has creator partnerships (Template 2 element); Gymshark has loyalty (Template 1 element); Alo has retail extensions (Template 1 element). The "primary axis" framing above identifies the dominant strategy, not the only one.

Is using public storefront screenshots fair use for editorial commentary?

Per US fair-use doctrine, transformative editorial commentary on publicly accessible commercial websites is generally protected. We avoid embedding storefront screenshots in this article specifically and link to the public URLs instead — readers can view directly. This is a stricter stance than legally required and reflects our editorial-content policy.

Will you cover other vertical comparisons?

Yes. Wave 3 includes Allbirds vs Veja vs Cariuma (sustainable footwear), additional fast-fashion vs DTC fashion comparisons, and more brand triples in adjacent categories. Existing comparison precedent: Allbirds vs Rothy's sustainable Shopify covers the two-brand comparison pattern in adjacent verticals.

Run the stack read on any Shopify brand

Install AliShopping Tools — Free on Chrome Web Store

The classification, app-stack, and live-sales reading we used in this article is the same surface available on every Shopify storefront you visit. Open any Shopify-hosted brand and run the three-axis read for yourself. Free, one click, public-data only.

Ready to find winning products?

Try AliShopping Tools — 15 free AI tools for product research.

Quick answers

Frequently Asked Questions

1Are Lululemon, Gymshark, and Alo Yoga on Shopify?

Yes, all three use Shopify as their e-commerce platform.

Despite being the highest-profile fitness apparel brands, they run on Shopify's infrastructure with radically different app stack strategies.

Lululemon optimizes for retail-omnichannel integration, Gymshark for community-creator velocity, and Alo Yoga for premium aesthetic and lifestyle adjacency.

2What can indie operators learn from Lululemon's Shopify stack?

Lululemon's stack shows how to integrate offline retail with online DTC through loyalty programs and omnichannel inventory management.

The retention infrastructure — loyalty points, store credit, personalization — represents a mature customer LTV strategy.

Indie operators can borrow the loyalty-first acquisition model even at smaller scale using off-the-shelf apps.

3What is different about Gymshark's Shopify strategy vs Alo Yoga?

Gymshark optimizes for creator-content velocity and community activation — their stack reflects fast content production and influencer program infrastructure.

Alo Yoga optimizes for premium aesthetics and lifestyle positioning — their stack reflects editorial content tools and high-end photography workflows.

The same Shopify platform serves fundamentally different brand strategies.

4How do these premium brands use Shopify differently from dropshippers?

Premium brands like Lululemon and Gymshark build proprietary or custom apps on top of Shopify — systems for loyalty, fulfillment at scale, and community management that dropshippers cannot access off the shelf.

The cost of their tech stack alone exceeds what most solo operators spend annually.

Standard Shopify is the shared foundation; the divergence is in what is built on top.

More from the blog

Gymshark vs Alo Yoga: Shopify Strategy Breakdown

Gymshark vs Alo Yoga Shopify strategy — full app stack, theme, pricing psychology, ad approach decoded. Free 1-click reveal of both brand stacks. Case study.

Allbirds vs Rothy's: Sustainable Shopify Breakdown

Allbirds vs Rothy's Shopify breakdown — sustainable DTC playbook, app stack, pricing strategy, storytelling tactics decoded. Free 1-click stack reveal.

Fashion Nova vs PrettyLittleThing: Shopify Tactics

Fashion Nova vs PrettyLittleThing Shopify tactics — fast-fashion playbook, drop cadence, influencer model, and pricing psychology decoded. Free store reveal.